From buying a cup of coffee to purchasing a flight ticket, these little plastic cards make our lives convenient. But have you ever wondered what happens behind the scenes when you swipe or insert your card? In this guide to credit card processing learn the players involved and how this process gets money from the customer into your business account.

The Intricacies of Credit Card Transactions

Understanding the intricacies of credit card transactions isn’t just for the tech-savvy or those in the finance industry. It’s crucial for both businesses and consumers. For businesses, a clear grasp of this process can help in choosing the right partners, optimizing transaction fees, and ensuring customer satisfaction. For consumers, it demystifies what happens to their money and provides insights into potential fees, privacy, and security.

Key Entities in Credit Card Processing

Understanding the intricacies of credit card transactions isn’t just for the tech-savvy or those in the finance industry. It’s crucial for both businesses and consumers. For businesses, a clear grasp of this process can help in choosing the right partners, optimizing transaction fees, and ensuring customer satisfaction. For consumers, it demystifies what happens to their money and provides insights into potential fees and security measures.

1. Merchant

Who are they?

The merchant is any business or individual that sells goods or services. Whether it’s your favorite coffee shop or an online store, they are merchants.

Role in the Process:

Merchants initiate the credit card transaction process when a customer decides to make a purchase. They use a point-of-sale system or an online gateway to capture the card’s details and request payment authorization.

2. Cardholder

Who are they?

A cardholder is the customer. They are the individual or entity that holds a credit card.

Role in the Process:

The cardholder initiates a transaction by presenting their card for payment. They also have the responsibility of ensuring they have sufficient credit and are aware of their card’s terms and conditions.

3. Merchant's Bank

Who are they?

The merchant’s bank is a financial institution that maintains the merchant’s business account.

Role in the Process:

The merchant’s bank receives the payment authorization request from the merchant and forwards it to the payment processor. Once approved, they credit the merchant’s account with the transaction amount, minus any fees. Ultimately this is where the customer’s money finalizes.

4. Payment Processor

What’s the difference between Merchant Banks and Third-Party Processors?

The Payment Processor is a company used by the merchant to manage transactions from various channels, such as credit and debit cards.

Role in the Process:

The payment processor acts as a mediator, facilitating the communication between the merchant, issuing bank, and card associations. They ensure the transaction is authenticated, authorized, and settled.

Examples Of Credit Card Processors

5 .What is a Credit Card Processing Gateway?

Who are they?

A credit card processing gateway is a service or platform that securely transmits transaction data between merchants and payment processors or banks. They are the digital intermediaries that ensure the safe and efficient handling of online credit card transactions.

Role in the Process:

In essence, the credit card processing gateway acts as the bridge between the merchant and the financial institutions, ensuring that online transactions are carried out securely and efficiently.

6. Card Associations

Who are they?

Card associations are organizations like Visa, MasterCard, American Express, and Discover.

Role in the Process:

These associations set the rules and standards for credit card transactions. They also act as a gateway between the payment processor and the issuing bank, ensuring that transactions adhere to their guidelines. Additionally, they’re responsible for determining interchange fees, which are transaction fees that the merchant’s bank pays to the issuing bank.

7. Issuing Bank:

Who are they?

The Issuing Bank is the financial institution that provides the cardholder with their credit card. They are responsible for verifying the cardholder’s credit and either approving or declining transactions.

Role in the Process:

When a transaction is initiated, the issuing bank verifies the cardmember’s credit and either approves or declines the transaction based on available credit, potential fraud, or other factors. If approved, they will later bill the cardmember for the transaction.

Common Misconception:

It’s a widespread misconception that card associations like Visa or MasterCard are the issuing banks. In reality, they are not banks and do not issue credit cards to consumers. Instead, they provide the infrastructure and set the standards for credit card transactions. Examples of issuing banks include JPMorgan Chase, Bank of America, Wells Fargo, and Citibank, among others.

In contrast to the above, American Express and Discover are unique in the credit card industry because they operate as both card associations and issuing banks. This means they not only set the rules and standards for their credit card transactions but also directly issue credit cards to consumers.

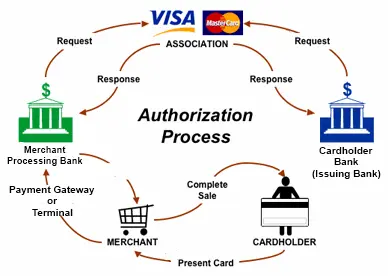

How Does A Credit Card Transaction Work?

Every credit card transaction goes through a series of steps, starting with the cardmember providing their card details and culminating in the merchant receiving payment. This process is where the transaction gets the green light to proceed. It ensures that the cardmember has sufficient funds or credit available and that the transaction is legitimate. Here’s a detailed breakdown: While it is intricate this all happens within a few sections. Each step is crucial, ensuring the transaction is accurate, secure, and efficient.

Authorization

1. Card Holder Initiation

The cardmember provides their credit card details for a purchase, either by swiping, inserting, tapping, or manually entering them online.

2. Transaction Data Capture

The merchant’s POS system or online payment gateway captures the transaction details, including card number, expiration date, CVV, and transaction amount.

3. Data Transmission to Processor

The captured details are sent to the merchant’s payment processor.

4. Authentication

Before forwarding the transaction details for authorization, the payment processor initiates the authentication process. This step verifies the legitimacy of both the card and the cardmember. It checks the card’s security features, such as the CVV or chip, and may validate the cardmember’s identity through additional measures like a PIN, signature, or even two-factor authentication for online transactions.

5. Request to Card Association

Post-authentication, the payment processor sends the transaction details to the relevant card association (e.g., Visa, MasterCard).

6. Routing to Issuing Bank

The card association routes the transaction request to the issuing bank associated with the cardmember’s credit card.

7. Transaction Verification

The issuing bank checks the transaction details, ensuring the cardmember has enough credit or funds, and scans for potential fraud or security flags.

8. Approval or Decline

Based on the verification, the issuing bank sends back a response. If approved, an authorization code is provided. If declined, a reason is given.

9. Response to Merchant

The response is sent back through the card association and payment processor to the merchant.

10. Completion

If the transaction is approved, the merchant completes the sale, and the cardmember’s account is earmarked for the transaction amount. The actual transfer of funds occurs later during the settlement process.

Settlement

The settlement is the final step where the merchant receives the funds from the transaction. This involves the issuing bank transferring the transaction amount, minus any fees, to the merchant’s bank. An essential fee to understand here is the ‘interchange fee’, a charge paid by the merchant’s bank to the cardmember’s issuing bank.

Why Transactions Might Be Declined

Credit card transactions can face hiccups for a myriad of reasons. While some are straightforward, others might require a deeper dive. Here’s a list of the most common culprits:

Insufficient Funds:

Perhaps the most common reason. If the cardmember doesn’t have enough money in their account or has reached their credit limit, the transaction will be declined.

Expired Card:

If the card’s expiration date has passed, it won’t be accepted for transactions.

Incorrect Card Details:

Mistyped card numbers, wrong expiration dates, or incorrect CVV codes can lead to declines, especially in online transactions.

Suspicious Activity:

Banks and credit card companies have systems in place to detect unusual patterns or behaviors that might indicate fraud. If a transaction seems out of the ordinary, it might be flagged and declined.

Holds or Freezes:

If there’s a hold on the cardmember’s account or if the account has been frozen due to reasons like suspicious activity or unpaid dues, transactions will be declined.

Technical Glitches:

One of the more popular causes; Sometimes, the issue isn’t with the cardmember or the merchant but with the technology. Wifi(!!) POS system malfunctions, issues with the payment gateway, or even temporary server downtimes can result in declined transactions.

International Transactions:

Some cards have restrictions on international transactions. If a cardmember tries to make a purchase from a foreign country or in a foreign currency without prior notification, it might be declined.

Overactive Fraud Detection:

While fraud detection is crucial, sometimes systems can be overly cautious, declining legitimate transactions that seem slightly out of the norm.

Daily Limit Exceeded:

Some cards have daily spending limits. If a cardmember exceeds this limit, subsequent transactions might be declined until the next day.

Card Not Activated:

New cards or replacement cards need to be activated before use. If not activated, they’ll be declined.

Understanding these reasons is beneficial for both merchants and cardmembers. For merchants, it helps in addressing customer concerns promptly and efficiently. For cardmembers, it provides clarity and can guide actions to prevent future declines.

Conclusion

Understanding the credit card transaction process is essential for businesses and consumers alike. With Fusion Payments, you’re not just getting a service provider; you’re gaining a partner committed to ensuring your transactions are optimized. Join us on this journey to redefine the credit card experience.

Should My Bank be My Credit Card Processor?

At first glance, it may seem like your bank is the most convenient choice for being your credit card processor. After all, they handle your business accounts, loans, and other financial needs. It feels natural to assume they’d be the best fit for your credit card processing needs as well. However, in many scenarios, this is just not the case.

Fusion Payments offers a distinct advantage over traditional bank processing. Here’s why:

- Tailored Solutions: Every business is unique, and so are its payment processing needs. Unlike banks that often offer generic solutions, we customize our services to fit the specific requirements of your business, ensuring you get the most efficient and cost-effective processing solution.

- Advanced Technology: The world of payment processing is evolving rapidly. We stay ahead of the curve, implementing the latest technological advancements, ensuring your transactions are not only fast but also secure.

- Transparent Pricing: Hidden fees and unexpected charges can be a real pain point with traditional bank processing. At Fusion Payments, our pricing is transparent. You’ll always know what you’re paying for, with no unpleasant surprises.

- Dedicated Support: Our commitment to our clients goes beyond just providing services. We offer dedicated support, ensuring any queries or issues are addressed promptly. With banks, you might find yourself lost in a maze of automated responses and long wait times.

Don’t just take our word for it; our satisfied clients vouch for our excellence. They’ve experienced the Fusion Payments difference and have seen firsthand how we stand head and shoulders above traditional bank processing.